Iron & Steel

Navigating the Chromium Supply Chains | MetalshubTalks 008 Recap

Published on

Share Post

Iron & Steel

Published on

Share Post

Chromium rarely gets the mainstream spotlight compared to other metals like copper or lithium, yet it serves as the invisible backbone of modern industrial stability. As the foundational element that gives stainless steel its corrosion resistance and high-temperature durability, chromium is deeply embedded in strategic sectors ranging from aerospace and defence to medical technologies and green energy infrastructure.

In a recent episode of MetalshubTalks, I sat down with Sheraz Neffati, Executive Director of the International Chromium Development Association (ICDA), and Dr. Sebastian Kreft, Co-Founder and Managing Director at Metalshub. They explored how shifting regional dynamics, the rollout of the EU Carbon Border Adjustment Mechanism (CBAM), geopolitical friction, and artificial intelligence are fundamentally rewriting the rulebook for the global chromium value chain.

Chromium is essential to global stainless steel production, yet it often receives far less attention than other raw materials. From the ICDA’s perspective, how do you view chromium’s strategic importance today?

Sheraz Neffati: Chromium is undeniably critical. To date, it remains the only element without a true substitute that provides stainless steels and high-performance alloys with corrosion resistance, mechanical strength, and stability under extreme temperatures. This makes it vital for national security, infrastructure, and industrial stability.

NATO classifies chromium as highly critical for military applications, and nations like the US, Canada, China, Japan, Russia, and India have officially designated it as a critical or strategic material. Interestingly, the EU has not yet re-classified chromium as critical or strategic, despite having done so in the past. I would therefore unambiguously consider chromium to be both critical and strategic.

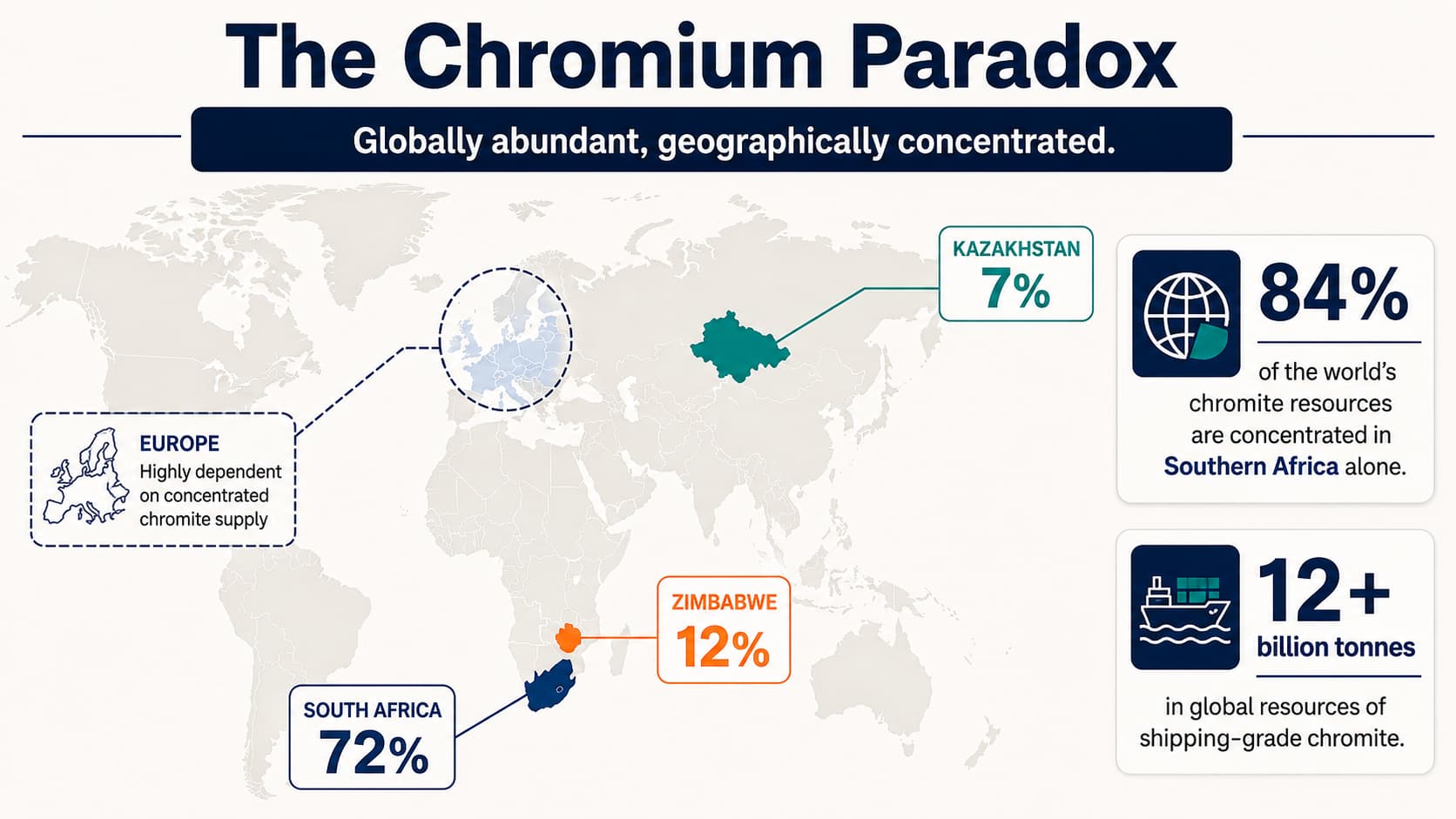

A key paradox is that chromium is globally abundant—with resources exceeding 12 billion tonnes of shipping-grade chromite—yet its geographic concentration is incredibly tight. Roughly 72% of global chrome ore resources are located in South Africa, 12% in Zimbabwe, and 7% in Kazakhstan. That means roughly 84% of the world’s chromite resources sit in Southern Africa alone. This extreme concentration exposes downstream consuming regions, particularly Europe, to massive supply chain vulnerabilities if local logistics or energy grids fail.

South Africa has historically dominated global ferrochrome production, but structural challenges like energy costs have severely pressured its position. How is its role evolving?

Sheraz Neffati: The market simply cannot decouple from South Africa due to its 72% share of ore reserves. However, its competitiveness as a refined ferroalloy producer has suffered severely over the last decade. Power utility Eskom’s tariffs have risen approximately tenfold, alongside persistent power shortages and socioeconomic instability.

Consequently, South Africa’s installed ferrochrome capacity shrank from 6.5–7 million tonnes in the mid-2010s to just 4.7 million tonnes by 2025, consolidating down to just two integrated market players: Glencore-Merafe and Samancor Chrome.

Where has that displaced production capacity gone?

Sheraz Neffati: It has moved straight to China and Indonesia. China has rapidly expanded its domestic ferrochrome production capacity from 13.8 million tonnes in 2019 to 18.3 million tonnes in 2025. Since China has virtually zero domestic chromium resources in its own soil, it now imports 90% of South Africa’s raw chrome ore.

Crucially, China does not export ferrochrome; it applies a 40% export duty to keep the material inside its borders, turning it into stainless steel and finished goods. Together, China and Indonesia now command 64% of global ferrochrome production. For Europe, this represents a structural squeeze, cutting off direct access to raw material alternatives and increasing reliance on highly concentrated external market dynamics.

We are also hearing a lot about Zimbabwe’s ambitions to move from an ore exporter to a refined ferrochrome producer. What is the reality on the ground there?

Sheraz Neffati: Zimbabwe is already an active ferrochrome producer with 43 operating furnaces and an annual capacity of nearly 790,000 tonnes. However, it remains heavily integrated with China; in Q1 2026, nearly 100% of Zimbabwe’s raw chrome ore exports went directly to China.

Many upcoming projects are majority-owned by Chinese entities, reflecting strong diplomatic and economic ties. The most ambitious example is the US$ 3.6 billion “Pal River” project in the Beitbridge area, being developed by a major Chinese producer. The final phase aims for 1 million tonnes of stainless steel and up to 2 million tonnes of ferrochrome capacity vertically integrated with localised coking plants and power stations.

Dr. Sebastian Kreft: When we visited Zimbabwe recently for the ICDA Africa Chromium Week, the government’s ambition and commitment to local value addition and processing were incredibly clear. However, the country faces two primary bottlenecks:

The EU Carbon Border Adjustment Mechanism (CBAM) is now fully operational. What does this mean practically for chromium producers operating outside of Europe?

Sheraz Neffati: It is important to emphasise that CBAM does not currently cover raw chrome ore; its focus is on refined ferrochromium. The policy’s goal is to protect European ferroalloy producers who have invested heavily in greening their production by imposing a carbon cost on imports coming from regions with looser environmental regulations.

Because of this, Environmental Product Declarations (EPDs) and Life Cycle Assessments (LCAs) are becoming vital commercial tools. Kazchrome, for instance, successfully secured an EPD recently, following companies like Outokumpu and Tata Steel. Outside compliance, this data helps companies prove their actual footprint directly to international buyers.

Dr. Sebastian Kreft: CBAM completely shifts the commercial landscape. Because standard stainless steel contains roughly 18% chromium, the carbon footprint of the alloy you buy heavily influences the final footprint of the steel.

For the very first time, non-EU ferrochrome producers have an immediate economic incentive to invest in renewables and decarbonisation. If they import carbon-heavy material into Europe, they face severe financial penalties that erode their competitiveness.

How do you see the global competitive dynamics playing out under CBAM over the long run?

Sheraz Neffati: My personal view is that CBAM is a reactive measure rather than an anticipatory one. Look at the speed of China’s energy transition: Inner Mongolia, which accounts for over 75% of Chinese ferrochrome output, is now China’s top renewable energy hub. Renewable energy already accounts for more than half of the region’s installed capacity. By 2030, they aim for clean energy to hit 65% of installed capacity.

China is moving aggressively to ensure its long-term energy security while scaling low-carbon manufacturing. If European frameworks only look at today’s challenges, they may find themselves unprepared when foreign suppliers begin exporting low-carbon alloys that easily bypass carbon tariffs altogether.

Sebastian, Metalshub frequently highlights digitalisation as a requirement for survival in modern metals procurement. Where can artificial intelligence realistically improve chromium supply chains over the next decade?

Dr. Sebastian Kreft: We are still in the early stages of industrial AI adoption, but the velocity is accelerating. In the chromium space, we focus heavily on two highly practical use cases:

The insights shared in this episode make it explicitly clear that the global chromium market is navigating a complex structural transition. Supply chains can no longer rely on traditional geographic distribution or historical trade patterns.

For procurement professionals and industrial consumers to protect their supply lines, strategic focus must shift toward three core initiatives:

MetalshubTalks 008

Interested in watching the full episode?

Click below and watch it for free.

insights