Battery Raw Materials

Cobalt Market Dynamics: Supply, Demand, and the Challenge of Price Discovery

Published on

Share Post

Battery Raw Materials

Published on

Share Post

Cobalt is often described as a strategic material for the energy transition, due to its role in lithium-ion batteries, aerospace alloys, and other high-performance applications. Yet, unlike many industrial metals, cobalt does not have a single, clearly defined global market price. Many transactions are priced as payables linked to benchmark references, with adjustments for specifications, processing routes, and delivery terms. As demand grows with electric vehicles and energy storage, while supply remains highly concentrated, this structure makes it difficult to assess where cobalt is truly trading. As a result, the industry is increasingly looking for more transparent and comparable price signals beyond traditional benchmarks.

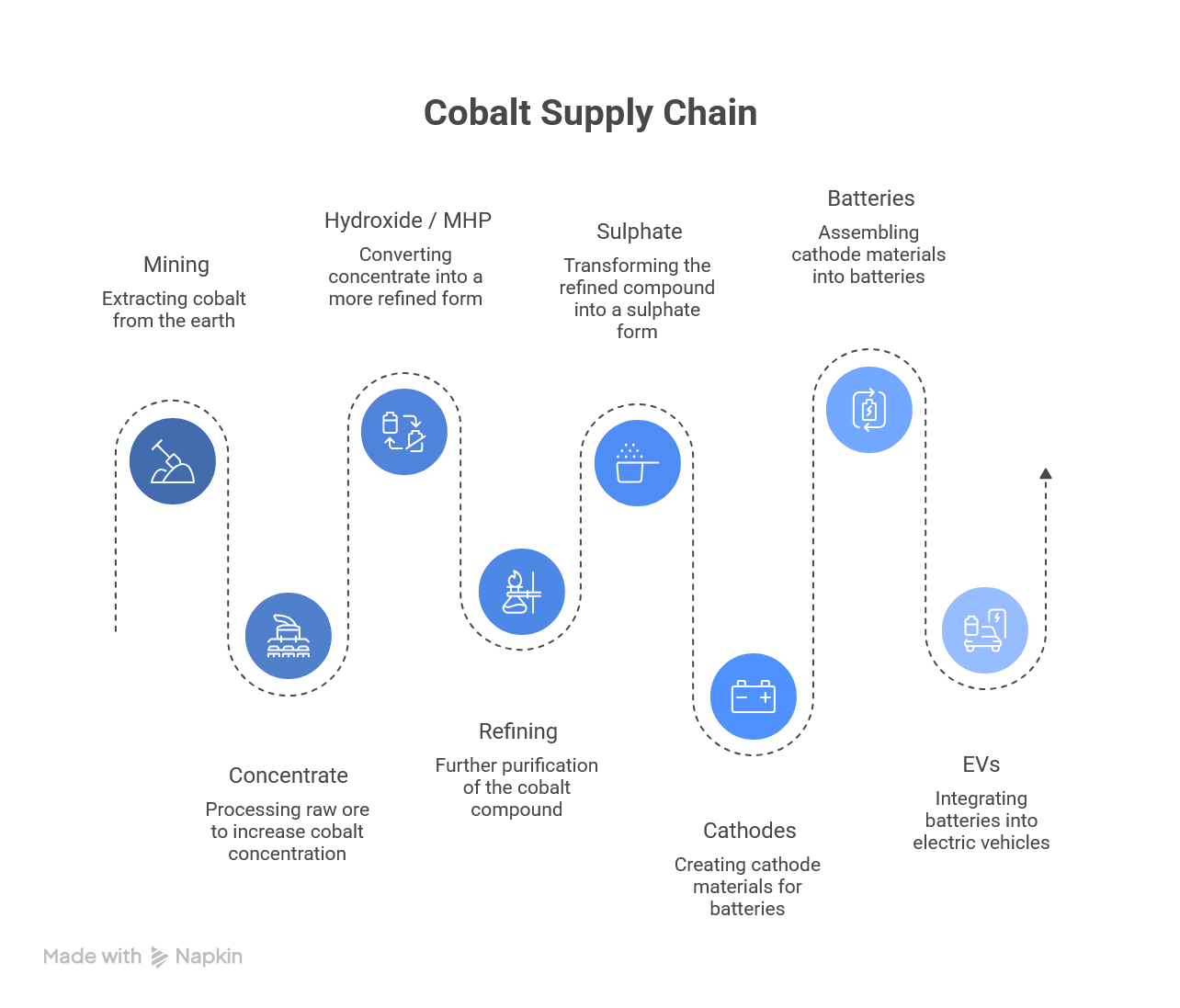

Cobalt’s value chain is unusually multi-form. Even within a single price-reporting framework, separate assessments exist for different cobalt products, such as standard-grade metal, alloy-grade metal, cobalt hydroxide, cobalt sulphate, and cobalt tetroxide, each with different delivery locations and timing conventions.

Figure 1. The cobalt supply chain from mining and concentrate processing to intermediates, cathodes, and applications

A key structural feature is that many transactions are priced as payables rather than flat prices. Instead of quoting a direct unit price for cobalt units, intermediates such as cobalt hydroxide are commonly priced as a percentage of a cobalt metal benchmark.

Specifications and impurities directly affect pricing. Intermediates such as cobalt hydroxide are traded with strict chemical requirements, including minimum cobalt content and maximum impurity levels. Elements such as manganese, magnesium, sulphur, and cadmium can materially affect payables and cargo acceptance. Additional constraints, such as radioactivity limits for imports into China, can further influence pricing outcomes.

The downstream processing route also shapes pricing:

Demand is not purely battery-driven. In the United States, superalloys accounted for about 51% of cobalt consumption in 2025, followed by chemical applications at roughly 25%.

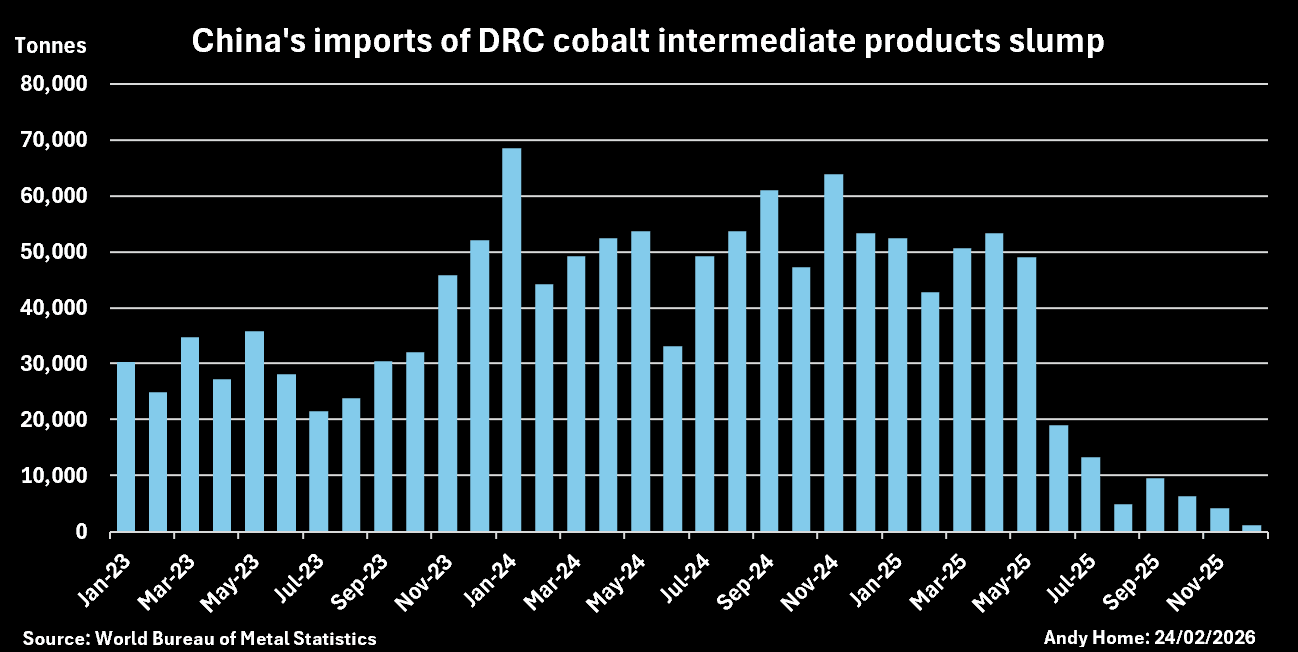

Figure 2. China’s DRC cobalt imports plunge in 2025. Credit: Reuters

As a result, many end-users never buy refined cobalt metal directly. Battery and precursor producers usually purchase chemical intermediates linked to metal benchmarks, reinforcing a pricing system based on formulas, specifications, and processing routes.

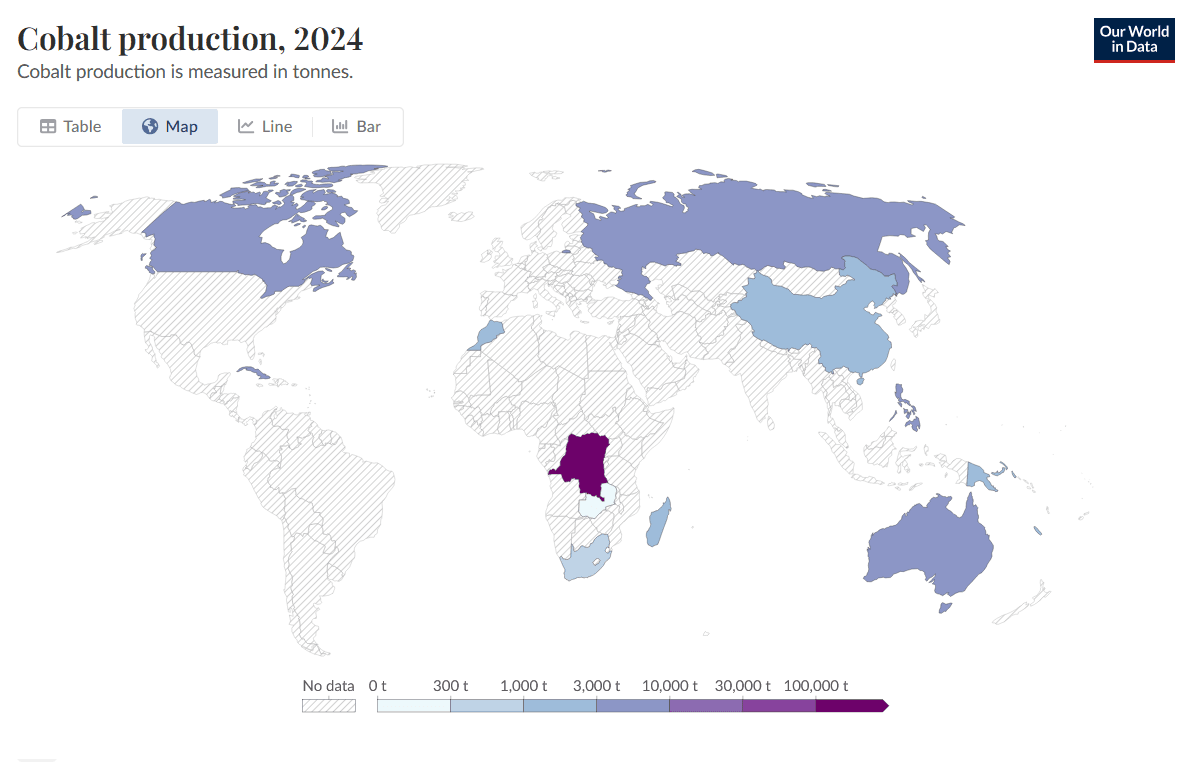

Cobalt supply is unusually concentrated, which makes geopolitical developments a constant variable in pricing discussions. According to the USGS, the Democratic Republic of the Congo (Congo-Kinshasa) produced about 73% of global mined cobalt in 2025, far ahead of the next largest producer, Indonesia, at roughly 14%.

Figure 3. Global cobalt production is concentrated in the DRC. Credit: Our World in Data (Last Updated: June, 2025)

The USGS estimates 230,000 tonnes of cobalt mine output in Congo-Kinshasa in 2025, out of a global total of around 310,000 tonnes. This means the majority of global cobalt supply originates from a single jurisdiction, a level of concentration rarely seen across major industrial metals.

China’s dominance lies primarily in refining and chemical conversion, rather than in mining. Cobalt ore and intermediates are largely mined in Central Africa, shipped globally, and then processed in Chinese refineries before entering battery and chemical markets. Analysis citing the International Energy Agency indicates that China accounted for approximately 78% of global refined cobalt production in 2024.

Because of this structure, disruptions do not always appear first in the headline metal prices. Restrictions or disruptions at the mining stage can tighten availability of intermediates such as cobalt hydroxide, pushing payables higher and squeezing refiners long before refined metal benchmarks fully reflect the change.

Recent price movements in the cobalt market have been shaped less by demand and more by policy interventions.

In February 2025, the DRC government temporarily banned cobalt exports to address oversupply and falling prices. By October 2025, the ban was replaced with a quota system limiting exports to 18,125 tonnes for the remainder of 2025 and up to 96,600 tonnes annually in 2026–2027, including 9,600 tonnes allocated to national strategic reserves.

Implementation delays added friction. Export shipments under Q4 2025 quotas were allowed to proceed until March 2026, and producers faced additional administrative steps before cargoes could leave the country. Quota allocations for major producers included CMOC (6,650 tonnes) and Glencore (3,925 tonnes).

Between February and December 2025, CME cobalt metal rose from roughly $10/lb (≈$22,000/mt) to $26/lb (≈$57,000/mt), while cobalt hydroxide increased from about $6/lb (≈$13,000/mt) to $23/lb (≈$51,000/mt). Market reports also described hydroxide payables reaching 100% of the metal benchmark, highlighting a tight intermediate market.

Two structural features of the cobalt market amplified the impact:

While recent price movements have been driven largely by supply-side interventions, demand growth in cobalt remains positive, but the structure of that demand is changing. Growth is increasingly segmented by battery chemistry choices and regional market preferences, which is reshaping how cobalt consumption evolves over time.

The Cobalt Institute’s Q4 2025 market update estimated total cobalt demand at around 213.5 kt in 2025, with growth revised down to approximately 3% year-on-year. Demand is expected to reach roughly 219.6 kt in 2026, reflecting a recovery to around 7% growth. Electric vehicles remain the largest incremental driver, although demand expectations have softened due to a weaker EV outlook in key markets. Outside batteries, superalloy demand continues to expand, supported by steady growth in aerospace and industrial applications.

Battery chemistry trends are influencing cobalt intensity. In China, EV manufacturers have increasingly adopted lithium-iron-phosphate (LFP) batteries, which contain neither cobalt nor nickel. Market analysis suggested LFP could grow from 48% of global vehicle battery share in 2024 to about 65% by 2029. The same reporting noted that the average cobalt used in new passenger vehicles had already fallen to roughly 2.2 kg per vehicle (depending on battery chemistry), down about 6% year-on-year.

Western EV markets, particularly in North America, still rely heavily on nickel–cobalt chemistries such as NCM, which offer higher energy density and longer driving range. Vehicles using these batteries often carry larger battery packs, increasing overall materials demand even as cobalt intensity per kWh gradually declines.

Battery manufacturers are also exploring sodium-ion technologies as a potential alternative to lithium-ion systems, while academic research comparing NMC and LFP batteries highlights differences in cost, performance, and life-cycle impacts.

Cobalt pricing increasingly operates with multiple benchmarks rather than a single reference price. In practice, market participants rarely ask “what is the cobalt price?” Instead, they ask about which product, in which location, and linked to which benchmark.

Price reporting frameworks reflect this structure. For example, Fastmarkets publishes separate assessments for key cobalt products, each with distinct commercial conventions:

Pricing relationships between these products are formula-based. In practice, the inferred hydroxide price is calculated by multiplying the cobalt metal benchmark by the prevailing payable percentage, linking intermediate prices directly to the metal reference.

Pricing mechanisms can also shift depending on commercial conditions. Some supply contracts have alternated between European metal benchmarks and Chinese sulphate-linked pricing, reflecting where liquidity and demand signals are strongest at a given time.

Financial exchanges provide additional reference points but sit on top of this fragmented physical market. CME cobalt futures are financially settled using averages of Fastmarkets assessments, primarily supporting hedging and price transparency. Meanwhile, LME cobalt contracts are physically settled and include a designated liquidity window aimed at encouraging on-screen trading.

Taken together, these structural characteristics mean that cobalt price discovery remains fragmented and difficult to interpret consistently in real time. Multiple benchmarks, formula-based pricing, and limited spot liquidity leave market participants without a clear view of where cobalt is actually trading. This is where transaction-based data becomes critical.

Metalshub provides a digital infrastructure that enables structured transactions for raw materials, including cobalt intermediates and battery materials. While cobalt markets remain in the early stages of digitalisation, the same structural challenges around fragmented pricing, limited transparency, and formula-based transactions are already being addressed on the platform across other materials.

Each enquiry or offer on Metalshub captures the full set of commercial parameters that influence pricing, including:

By structuring these parameters within a single workflow, Metalshub makes it possible to compare offers on a like-for-like basis and generate more consistent price signals. As participation increases, this type of transaction data can provide a clearer view of how cobalt is priced in practice, particularly for intermediates where benchmarks alone are often insufficient.

Metalshub does not replace existing benchmarks, but complements them with structured bid and offer data that reflects real market conditions. This approach is designed to support more transparent and comparable price discovery as cobalt markets continue to evolve.

Book a demo to see how transaction-based insights from Metalshub can support better cobalt sourcing and pricing decisions.

Newsletter

insights