In the first quarter of 2026, the global urea market has been thrust back into the spotlight by a “perfect storm” of geopolitical and logistical shocks. As of April 2026, granular urea prices have surged to over $700 per metric tonne, a staggering 50% increase in just five weeks following the de facto blockade of the Strait of Hormuz. With nearly one-third of the world’s seaborne fertiliser trade and 40% of global urea exports passing through this single chokepoint, the market is currently navigating its most severe disruption since 2022.

Despite its size, the market does not operate around a single price, trading model, or transparent set of participants. Instead, it is shaped by regional imbalances, index-linked pricing, and fragmented visibility across counterparties. While prices react quickly to shifts in energy markets or geopolitics, commercial outcomes depend on more than price alone. A mix of long-term contracts, tenders, and spot transactions means that timing, logistics, contract structure, and counterparty access all play a critical role.

For a market that underpins global food security and sits at the critical intersection of energy economics and industrial demand, the urea market is a commercially complex ecosystem where execution, timing, and counterparty reliability are as critical as the price per tonne. This article explores the mechanics of how this market functions, why availability is not the same as accessibility, and how a layered approach to trading defines success in an increasingly fragmented world.

Key Takeaways

- Logistical Supremacy: A 95% collapse in commercial shipping through the Persian Gulf has narrowed the market’s focus on security of supply and reliable price discovery.

- The Access Gap: Supply availability no longer guarantees accessibility; regional bottlenecks and export restrictions mean “on-paper” supply is often trapped.

- Structural Layers: The market remains split between legacy producers locked into 95% long-term contracts (LTCs) and a fragmented, highly volatile downstream spot market.

- Infrastructure Gap: Reliance on manual workflows and fragmented communication continues to hinder transparent price discovery and efficient risk management.

Urea price in USD per metric tonne. Credit: Trading Economics

Why Urea Matters in the Global Fertiliser Economy

Urea is the backbone of the nitrogen fertiliser sector, favoured for its high nitrogen content (46%) and relative transport efficiency compared to other nutrients. Within the broader fertiliser market, currently valued at approximately $200 billion, urea stands out for its synthetic nature.

- The Energy Link: Unlike phosphate and potash, which are primarily mined mineral resources, urea is an industrial product linked directly to the Haber-Bosch process.

- Feedstock Sensitivity: Natural gas serves as both the primary feedstock and the energy source for production. Since urea synthesis consumes approximately 55% natural gas by volume, a 10% rise in gas prices typically translates to a 5% increase in production costs.

- Strategic Intersection: Consequently, urea sits at the volatile intersection of agricultural demand, natural gas supply, and global trade policy.

Despite this global importance, urea does not operate like an open, exchange-traded market. It remains a physical-first industry where bilateral trading is the norm, and most transactions are executed through contracts rather than liquid financial markets.

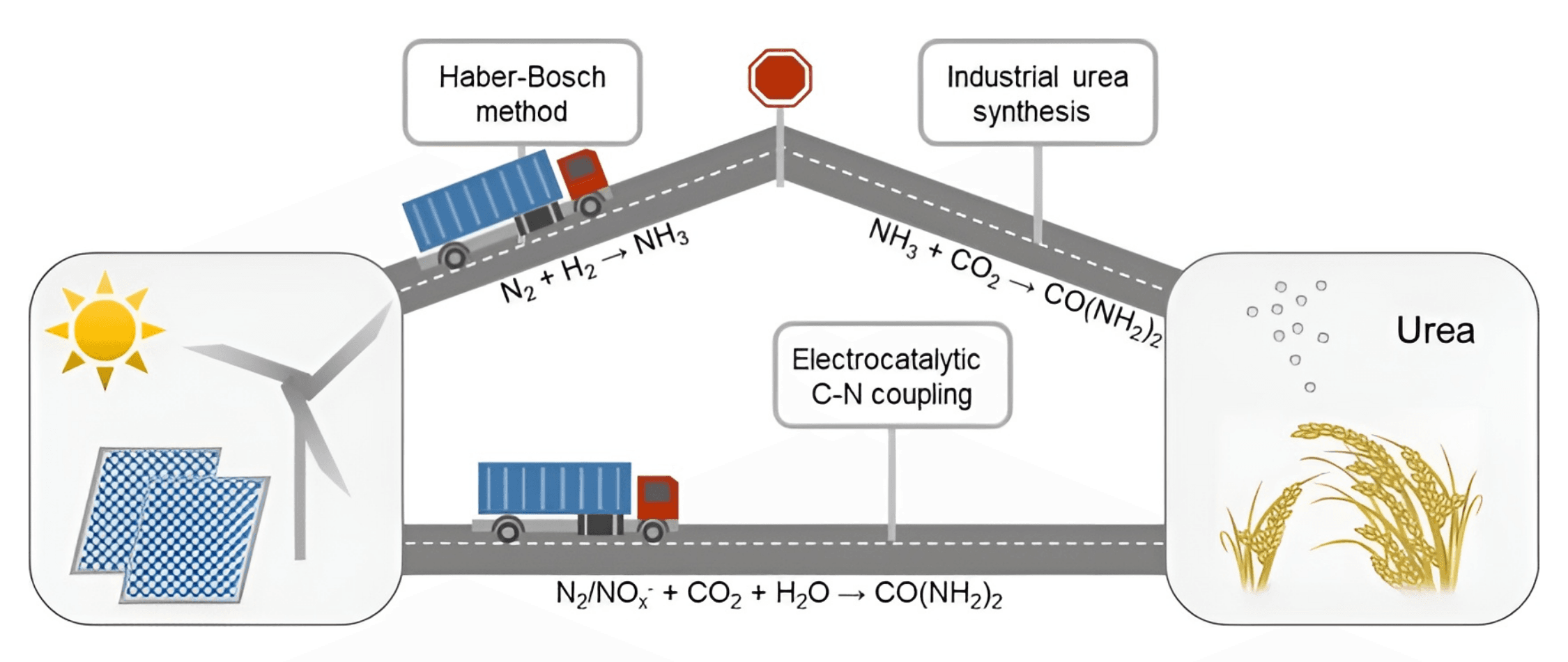

Pathways to urea synthesis: Haber–Bosch method combined with industrial urea synthesis (scenario A) and direct electrocatalytic C–N coupling process (scenario B). Credit: Chen et al., Small Science

A Global Market, But Not a Frictionless One

While urea is traded globally, it does not move with the fluidity of an exchange-traded financial asset. The market is defined by structural imbalances between production hubs and demand centres.

- Geographic Concentration: Production is dominated by gas-rich or large-scale industrial economies. China remains the world leader, projected to produce 76.5 million tonnes in 2026, followed by India, the Middle East, and the United States.

- Trade Flow Sensitivity: Demand is driven by seasonal planting cycles in the Northern Hemisphere and by large-scale agricultural nations such as Brazil and India. Because production is continuous but demand is episodic, the market relies on massive, well-timed trade flows.

- The Access Gap: Availability in the global market does not always translate into accessibility for buyers. Trade is frequently hampered by export restrictions, such as China’s recent prioritisation of domestic supply, and by geopolitical disruptions in critical corridors, such as the Strait of Hormuz. In fact, the shipping collapse through the Persian Gulf by over 95% in March 2026 has stranded millions of tonnes of production.

In this environment, “market price” can become secondary to “security of supply” Even when global supply is available, buyers face friction due to regional bottlenecks, port constraints, and the risk of counterparty default in a high-volatility environment.

Different Trading Layers, Not One Single Model

To understand urea, one must recognise that it is not a uniform market. Commercial behaviour varies significantly depending on where a participant sits in the value chain.

- Upstream (The Producers): Major miners and large-scale producers often operate with a “stability-first” mindset. Over 95% of their sales are frequently locked into long-term contracts (LTCs) lasting 1–5 years to ensure consistent supply. Digital affinity in this segment has historically been low, with contracts often stored as static PDFs on shared drives.

- Midstream (The Processors): NPK blending plants and processors—facilities that mix Nitrogen (N), Phosphorus (P), and Potassium (K) into customised formulas—operate on a hybrid model, often balancing a 50/50 split between LTCs for raw materials and spot sales for finished blends. This layer is the “engine room” of the market, where most of the complex “Excel-based” price calculations and margin management take place.

- Downstream (The Spot Market): Finished goods of fertiliser blends are almost entirely traded on a spot basis. This segment is highly fragmented, commercially dynamic, and the most exposed to immediate price volatility.

Understanding these layers is crucial. A “one-size-fits-all” digital solution would fail because it ignores the fact that a primary producer needs volume security, while a downstream distributor needs price discovery.

Urea fertiliser. Credit: Infinity Galaxy

Urea Prices are Referenced, Negotiated, and Adjusted

There is no single universal price for urea. Instead, the market operates through a series of regional benchmarks and price-reporting mechanisms. In 2026, up until the March surge, prices had hovered between $350 and $450 per tonne, but these figures are merely the starting point for negotiations.

A urea contract is rarely just about the price per tonne. It is a multi-variable equation that includes:

- Volume Optionality: The buyer’s right but not the obligation to call for additional tonnes based on regional demand

- Grade and Origin: Specific quality requirements that vary by jurisdiction

- Logistics: Freight terms (often CFR) and specific shipment windows (i.e. the laycan) that must align with vessel availability

Even when a deal is “index-linked,” the final commercial outcome is shaped by these variables. The lack of a central, transparent venue to compare these multi-dimensional offers remains a primary source of market opacity.

Logistics: The Active Constraint

Urea trading is inseparable from bulk logistics. Large sellers frequently manage shipments in Panamax-sized vessels, where the timing of the laycan must perfectly align with both the factory’s production schedule and the vessel’s arrival at the berth.

Operational stability is the highest priority for the world’s largest producers. Negotiating a trade is as much about vessel availability and loading constraints as it is about the price per tonne. This dependency means that a logistics failure—such as a port strike or a canal closure—is effectively a commercial failure.

Price Discovery: An Opaque Market

Despite the digital revolution seen in other sectors, urea trading remains surprisingly manual.

- Buyer search and counterparty access remain uneven: New producers or smaller sellers often struggle to access international markets, relying on a small circle of established traders or brokers. This limits competition and leaves buyers with fewer options during periods of supply stress.

- Commercial workflows remain manual: Despite the scale of the industry, many multi-million dollar deals are still coordinated via WhatsApp, phone calls, and Excel. This lack of structured data leads to:

- Documentation Friction: Handling origin certificates, quality reports, and compliance documents manually increases the risk of delay.

- Comparison Difficulty: It is hard to audit or compare historical performance when the deal data is trapped in individual email inboxes.

- Lack of Standardisation: Without a uniform framework for digital data exchange, every counterparty uses different templates and terms, making multi-party coordination inefficient.

- Compliance and documentation are becoming heavier: With the rise of carbon tax regimes and “green” ammonia initiatives, the documentation burden for product origin and environmental footprint is increasing, adding another layer of complexity to every trade.

This “digital immaturity” is not due to a lack of technology but to a lack of industry-specific, commercial infrastructure that can handle the specific complexities of the fertiliser trade and the resistance to change in a very traditional industry.

Hedging and the Liquidity Challenge

While a swaps market for urea exists via mechanisms like the CME or specialised fertiliser exchanges, liquidity remains imperfect. It can still take several days to exit a position, and the market often feels scattered as it remains highly broker-dependent. For many mid-sized players, the inability to hedge effectively is a major pain point that current market structures do not fully address.

What This Means for Buyers and Sellers in 2026

- For Buyers: Benchmark awareness is no longer sufficient for securing competitive margins. To achieve true price discovery, buyers must move beyond their “handful of known suppliers” and actively reach out to a broader cross-section of the market.

- Expanded Discovery: Relying on a small, closed network during a supply shock (like the 2026 Hormuz disruption) creates a single point of failure. Success now requires tools that allow buyers to broadcast requirements to a wider pool of vetted counterparties.

- Total Cost Analysis: Buyers need a structured way to compare total “landed” costs (CFR) rather than just headline FOB prices, accounting for the massive variations in current freight and insurance premiums.

- For Sellers: In an uncertain market, the ability to provide certainty is a value-added service.

- Market Access: For producers, the ability to quickly find and vet new international buyers is becoming a core competitive advantage.

- Execution Excellence: Sellers who can provide transparent, standard-format documentation and reliable vessel scheduling can command a “reliability premium.” When logistics are failing elsewhere, being the “easy to deal with” counterparty is a powerful differentiator.

The Path Forward: Better Commercial Infrastructure

As we look toward the rest of 2026 and beyond, the most realistic path to modernisation lies not in trying to force the entire market onto an exchange, but in providing structured digital workflows for the commercially complex midstream (processors) and downstream (spot market) layers.

The market increasingly requires:

- Clearer pricing references that form based on real bids, offers and transactions

- Broader counterparty access to ensure liquidity in times of crisis

- More structured commercial workflows across the transaction lifecycle, from offer comparison and negotiation to contract execution and documentation

The complexity of the urea market in 2026—driven by energy volatility, geopolitical tension, and layered trading behaviours—underscores the need for more robust commercial infrastructure. Transparency in this market comes from better processes, not a single reference price. It depends on how efficiently participants manage pricing, counterparties, and transactions. Metalshub aims to provide the digital infrastructure for these workflows.