Industrial Minerals

Battery Raw Materials

Rare Earth Supply Chain: Mines Are Not Enough Without Markets

Published on

Share Post

Industrial Minerals

Battery Raw Materials

Published on

Share Post

Rare earths have moved from niche industrial inputs to strategic materials at the centre of trade, defence, and industrial policy. Governments across North America, Europe, and Asia are racing to develop new mining projects, processing capacity, and downstream manufacturing for critical materials such as neodymium and praseodymium.

Yet for all the urgency around building non-Chinese supply chains, price discovery remains a critical and often overlooked gap in rare earth markets. In a market still shaped by fragmented specifications, limited spot liquidity, and Chinese price reference dominance, the challenge is no longer only how to produce rare earths, but also how to price them.

Rare earth elements (REEs) are a group of 17 metals used across advanced industrial technologies. Among them, neodymium, praseodymium, dysprosium, and terbium are essential for permanent magnets used in EV motors, wind turbines, robotics, defence systems, and consumer electronics.

These materials are traded in multiple product forms, including rare earth oxides (such as NdPr oxide), rare earth metals (NdPr metal, dysprosium metal), and magnet alloys used in permanent magnet production. Demand for these materials is expected to rise sharply as electrification accelerates.

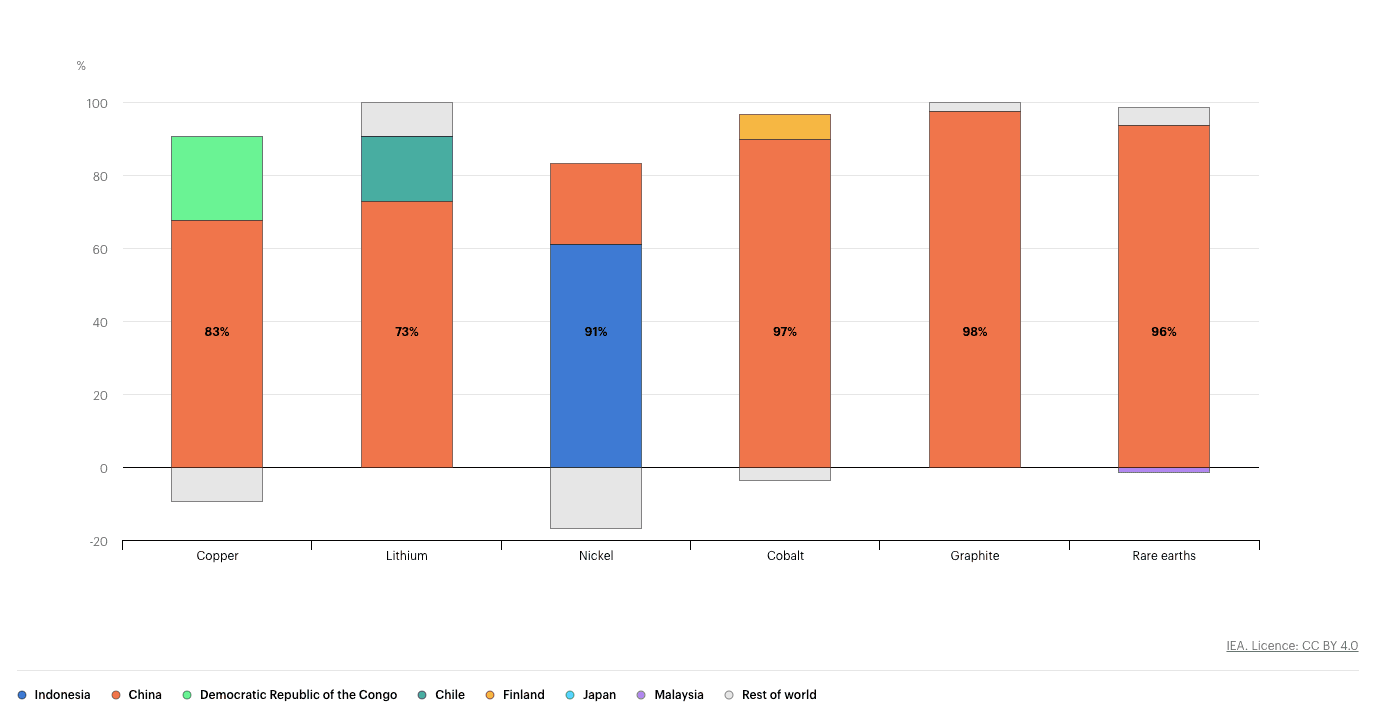

At the same time, supply chains remain heavily concentrated. According to the United States Geological Survey, global rare earth mine production reached approximately 390,000 tonnes of rare earth oxides (REO) in 2025, with China accounting for roughly 270,000 tonnes, or about 69% of global mine output.

China’s influence is even stronger in downstream processing, where most separation and refining capacity is located. This concentration has become a major strategic concern. Export controls and geopolitical tensions have prompted governments and industrial players to accelerate efforts to build alternative supply chains across North America, Europe, and Australia.

However, developing new supply does not automatically create a functioning market.

NdPr oxide prices in China (yuan per metric ton) have rebounded to ~850,000 yuan/mt (~$123,400/mt), highlighting recent volatility and policy-driven price support (Credit: Reuters).

Unlike metals such as copper or aluminium, rare earths are not traded on major commodity exchanges. The market lacks standardised contracts and universally accepted benchmarks.

Pricing varies widely depending on:

As a result, price discovery typically takes place through bilateral negotiations, tenders, and specialist price reporting agencies rather than through a transparent platform or exchange trading.

The market’s complexity is reflected in the number of price points needed to describe it. Fastmarkets, for example, publishes dozens of price assessments across different rare earth elements, grades, and regions. More recently, it has expanded its coverage to include new spot price assessments, reflecting growing demand for transparency and more representative pricing in evolving supply chains.

These developments mark an important step towards improved price visibility. However, they also highlight the market’s underlying fragmentation. In the absence of standardised products and liquid spot trading, price assessments remain dependent on a relatively limited set of transactions and negotiated deals.

This structure creates several challenges for market participants:

For a market that is becoming central to the global energy transition, this lack of pricing infrastructure is increasingly seen as a structural weakness.

Market participants across the rare earth value chain face different pricing challenges.

Without structured market interaction and comparable transaction data, each of these groups operates with limited price transparency and increased commercial uncertainty.

For decades, Chinese domestic prices have served as the dominant reference point for the global rare earth markets. Given China’s dominant role in both production and processing, this pricing structure reflected the realities of the supply chain.

Credit: IEA (2025), Change in refined copper, lithium, nickel, cobalt, graphite and rare earths production by country, 2020-2024, IEA, Paris https://www.iea.org/data-and-statistics/charts/change-in-refined-copper-lithium-nickel-cobalt-graphite-and-rare-earths-production-by-country-2020-2024, Licence: CC BY 4.0

But the emergence of new supply chains outside China is beginning to expose the limitations of this model.

As Reuters columnist Andy Home recently argued, Western countries need to build not only mines but also market infrastructure capable of supporting independent price discovery.

Non-Chinese rare earth supply chains operate under different economic conditions. Environmental regulations, permitting cycle times, and capital requirements differ significantly from those in China. These differences increasingly influence how buyers and producers evaluate supply contracts.

Market analysts have already begun observing potential “ex-China premiums”, particularly for heavy rare earth elements such as dysprosium and terbium, where processing capacity outside China remains limited.

As alternative supply chains expand, the need for transparent pricing mechanisms that reflect ex-China market conditions is likely to grow.

Credit: S&P Global

The foundations of price discovery in rare earth markets are closely linked to the development of new supply outside China. Projects such as Nolans, Eneabba, Browns Range, and the expansion of Mountain Pass and Mt Weld are expected to increase the availability of material into global markets and create the conditions for more active spot trading.

As new volumes enter the market, price discovery begins to emerge through more frequent transactions between buyers and sellers. In markets where liquidity is still developing, this activity is often fragmented and negotiated bilaterally, making it difficult to establish clear and comparable price signals.

Over time, more structured market interactions can help improve transparency. Competitive tenders, auctions, and standardised enquiry processes bring multiple participants into the same commercial setting, allowing prices to be tested across a broader range of bids and offers. This creates more comparable transaction data and supports the development of clearer market reference points.

This pattern has already been observed in other critical minerals markets.

Lithium markets, for example, saw increasing use of structured tenders and digital bidding events as producers sought clearer price signals during periods of rapid demand growth. These processes helped establish reference points for spot pricing and contract negotiations before more formal financial instruments began to emerge.

On Metalshub, structured tendering and standardised enquiry processes enable this type of market interaction in practice. By creating a comparable framework for bids and offers, they help generate clearer transactional signals and improve visibility in otherwise fragmented markets.

Rare earth markets may follow a similar path as supply chains diversify and liquidity develops outside China.

The rare earth sector is entering a period of structural change. Demand for rare earths used for magnets continues to rise as electrification accelerates across transport, energy, and industrial systems. At the same time, geopolitical pressures are driving efforts to diversify supply chains and reduce dependence on a single processing hub. Yet, building mines and refineries is only part of the solution.

Transparent pricing mechanisms, reliable benchmarks, and repeatable market processes are essential components of any mature commodity market. Without them, producers struggle to secure financing, buyers lack reliable price references, and policymakers face uncertainty when designing strategic supply chains.

For rare earths, the next stage of market development will depend as much on market infrastructure as on mineral resources.

In other words, the challenge facing the Western world is not simply to produce rare earths, but also to build the markets capable of pricing them.

Newsletter

insights